Canada’s top 100 retailers

March 4, 2020The CSCA Retail 100, created by the Centre for the Study of Commercial Activity at Ryerson University, brings you the top 100 retail organizations operating in Canada as ranked by total estimated annual retail sales in fiscal 2018/2019.

By Maurice Yeates and Tony Hernandez

CSCA’s Retail 100 listing has been augmented this year with a breakdown provided for both Retail Conglomerates (RCG) and the Retail Chains (RCH) that they control. A detailed understanding of this upper tier of retailers in Canada is important as these are organizations whose economies of scale allow them to exert a significant influence on Canada’s retail environment. The top 100 retail conglomerates account for close to 70 per cent of non-automotive retail sales in Canada in 2018, declining from 71.4 per cent in 2014. Considering the control they exert, understanding the marketing strategies and positioning that these top 100 retail players adopt provides insights into the ongoing processes that are continuously shaping Canada’s retail economy.

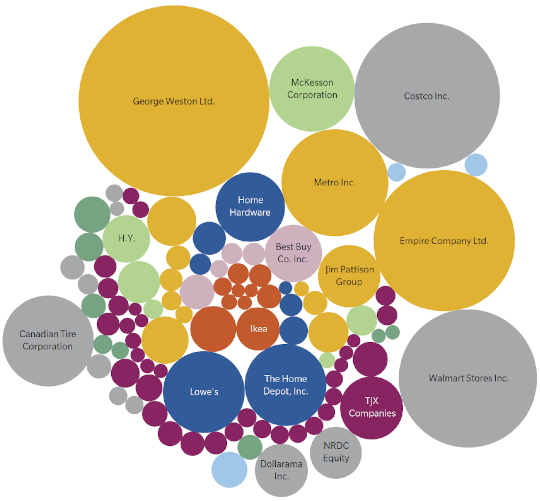

| RANK | CAPITAL CONTROL | CONGLOMERATE | EXAMPLE BANNERS | RETAIL SALES | SPACE SQUARE FEET | NO OF STORES | NUMBER OF CHAINS | DOMINANT NAICS CODE |

| 1 | CAN | George Weston Ltd. | Shoppers Drug Mart, The Real Canadian Superstore, Loblaws | 45,836 | 66,774 | 2,609 | 33 | 445 – Grocery |

| 2 | USA | Costco Inc. | Costco | 26,689 | 14,477 | 100 | 2 | 452 – General Merchandise |

| 3 | CAN | Empire Company Ltd. | Sobeys, Safeway, IGA, Farm Boy | 25,142 | 41,562 | 1,994 | 27 | 445 – Grocery |

| 4 | USA | Walmart Stores Inc. | Walmart Supercenters, Walmart | 24,012 | 60,402 | 411 | 2 | 452 – General Merchandise |

| 5 | CAN | Metro Inc. | Metro, Food Basics, Jean Coutu Pharmacy | 14,384 | 26,338 | 1,547 | 17 | 445 – Grocery |

| 6 | CAN | Canadian Tire Corporation | Canadian Tire, Mark’s Work Wearhouse, Sport Chek | 10,496 | 33,175 | 1,425 | 13 | 452 – General Merchandise |

| 7 | USA | McKesson Corporation | IDA Pharmacy, Uniprix, Rexall Drug Store | 9,192 | 9,848 | 2,343 | 11 | 446 – Health and Personal Care |

| 8 | USA | Lowe’s | Lowe’s, Rona, Rona Home & Garden | 8,418 | 24,671 | 649 | 9 | 444 – Home Improvement |

| 9 | USA | The Home Depot, Inc. | The Home Depot | 8,409 | 19,110 | 182 | 1 | 444 – Home Improvement |

| 10 | CAN | Home Hardware Stores Limited | Home Hardware, Home Hardware Building Centre | 6,100 | 12,305 | 1,076 | 4 | 444 – Home Improvement |

Major retailers dominate the ranking

A few large store-based conglomerates effectively control a large proportion of the current Canadian non-auto retail sales environment. Our latest data shows that this long-standing trend has continued apace. In 2018, the ten largest conglomerates controlled 48 per cent of national retail sales, increasing from 43 per cent in 2014.

The increasing retail dominance is focused on the largest retail conglomerates on the RCG100 list, as the overall contribution to national sales of all 100 retail conglomerates slightly decreased from 2014 to 2018.

Store closures and merger/acquisition activities have resulted in some major changes in the RCG100 listing over time. For example, seven conglomerate closures occurred between 2014 and 2018, involving $6.6b sales, of which Sears ($4.2b) and Target ($1.3b) were by far the largest. Mergers and acquisitions amongst ten conglomerates impacted $37.3b in sales, centred on four of the largest conglomerates in 2018 (Weston, Empire, Metro and McKesson).

Canadian retail control is shifting

Although Canadian headquartered companies provided the majority of sales (56.7 per cent) in the RCG100 in 2018, this share decreased by 3.4 percentage points from that in 2014. By contrast, stores headquartered in the US increased 1.9 percentage points, and in other countries by 1.5 percentage points. In 2018, 62.2 per cent of Canada’s non-auto retail sales were controlled by the RCH100.

The bulk of these sales are in groceries and beverage stores (20.3 per cent of national sales), general merchandise (17.8 per cent) and health and personal care (8.4 per cent). Groceries and beverage stores are dominated by Canadian headquartered chains. The general merchandise category is dominated by US headquartered operations. Health and personal care are dominated by Canadian headquartered businesses.

While the level of domination by the ten largest chains is about same for both 2014 and 2018, the 100 largest chains in 2014 contributed a greater share of national sales (65 per cent) than those in 2018. Thus, the difference in contribution to national sales between 2014 and 2018 is related to sales in chains ranked between 25th and 100th. Canadian headquartered chains contributed 6.4 percentage points less to the 2018 total than in 2014, while the contribution of chains headquartered in the US increased by 5.5 percentage points and from elsewhere in the world by 0.9 percentage points.

Burgeoning Online sales

Based on Environics Analytics’ ClickSpend data, it is estimated that the amount of online activity in 2018 in household expenditures for the main groups of retail – entertainment, electronics, clothing/shoes/children, sports & leisure, furniture & household, health & personal care, groceries/food/alcohol were $35.3b (i.e., 11.6 per cent of expenditures in these categories were spent online).

The highest shares of ‘online’ expenditure were in entertainment (30 per cent) and electronics (28 per cent). The lowest shares were in groceries/food/alcohol (less than 5 per cent). The ‘elephants’ in this non-auto retail sales ‘room’ are, of course, online e-retail activity – including pure-play (particularly via Amazon), direct-to-consumer (DtC) along with other eCommerce platforms. For example, Amazon’s estimated sales in Canada in 2018 were C$16.6b, which would place it as the 5th largest ‘retail conglomerate’ in the country! While the CSCA Retail 100 captures some of the online activities through store-based sales reporting of the retail conglomerates and their chains, much of the burgeoning e-retail sales are either not systematically reported or not reported at all. This remains an area in need of more data and research.

For more information concerning the CSCA Retail Top 100, or to download a full version of the report, visit the CSCA website.